Speak with an experienced advisor!

Speak with an experienced advisor! Buying life insurance policy when you have rheumatoid arthritis (RA) can feel like this:

Confusing and frustrating come to mind.

This is important – you can secure life insurance to protect your loved ones, even if you have rheumatoid arthritis.

The process may be easier than you think. If you have mild, or moderate at most, rheumatoid arthritis, no exam life insurance may be available to you.

If you have moderate to severe rheumatoid arthritis, not to worry. Life insurance options are always available.

What’s So Great About No Exam Life Insurance?

How To Prepare To Purchase A No Exam Policy

Apply For Life Insurance

What’s So Great About No Exam Life Insurance?

No exam life insurance has evolved. Not long ago, many life insurance carriers would have recommended against purchasing a non med (no exam) life insurance policy because it used to be cost prohibitive. Depending on your needs, the premium (what you pay in exchange for life insurance) amounts for no exam are competitive with their fully underwritten counterparts.

1. Price – competition amongst life insurance carriers has brought the price of no exam life insurance down. Today, premiums for no exam are often only slightly higher than fully underwritten policies. For comparison sake, check out two quotes. Here’s what you need to know:

- Phoenix Life Insurance Company offers no exam life insurance to those with rheumatoid arthritis. Not all carriers do.

- Prudential Financial’s quote is for fully underwritten life insurance, with a paramedical exam.

- The best health rating someone with rheumatoid arthritis can qualify for is standard.

- Life insurance quoters will often show a default health rating of preferred plus, displaying lower quotes than what those with RA would qualify for.

- The price differential between Phoenix (no exam) and Prudential (fully underwritten) is only approximately $6 per month.

2. Fast Approval – by skipping the paramedical exam, you can shave weeks off of your application process. If you are in a hurry to secure life insurance, no exam can be an excellent option. Reasons people opt for a fast approval include:

- They are going on vacation or traveling

- One less thing to worry about

- Divorce settlement

- Small business administration loan

- Spouse or partner keeps pressuring you to secure life insurance

3. Options – as more life insurance carriers offer no exam policies, your choices grow:

- Policy size (typically capped at $500,000)

- Term length (10 – 30 year terms)

- Approval for rheumatoid arthritis from select no exam carriers

4. Apply Online – your life insurance purchase process, from start to finish, can be accomplished online and over the phone. No need to leave your house.

5. No needles (or nurses!) – while your rheumatologist may regularly monitor your liver function and inflammatory markers with blood draws, for some of us, one less poke is fantastic. Here’s what you will avoid by skipping medical underwriting:

- blood draw

- urine sample

- blood pressure measurement

- pulse

- height and weight

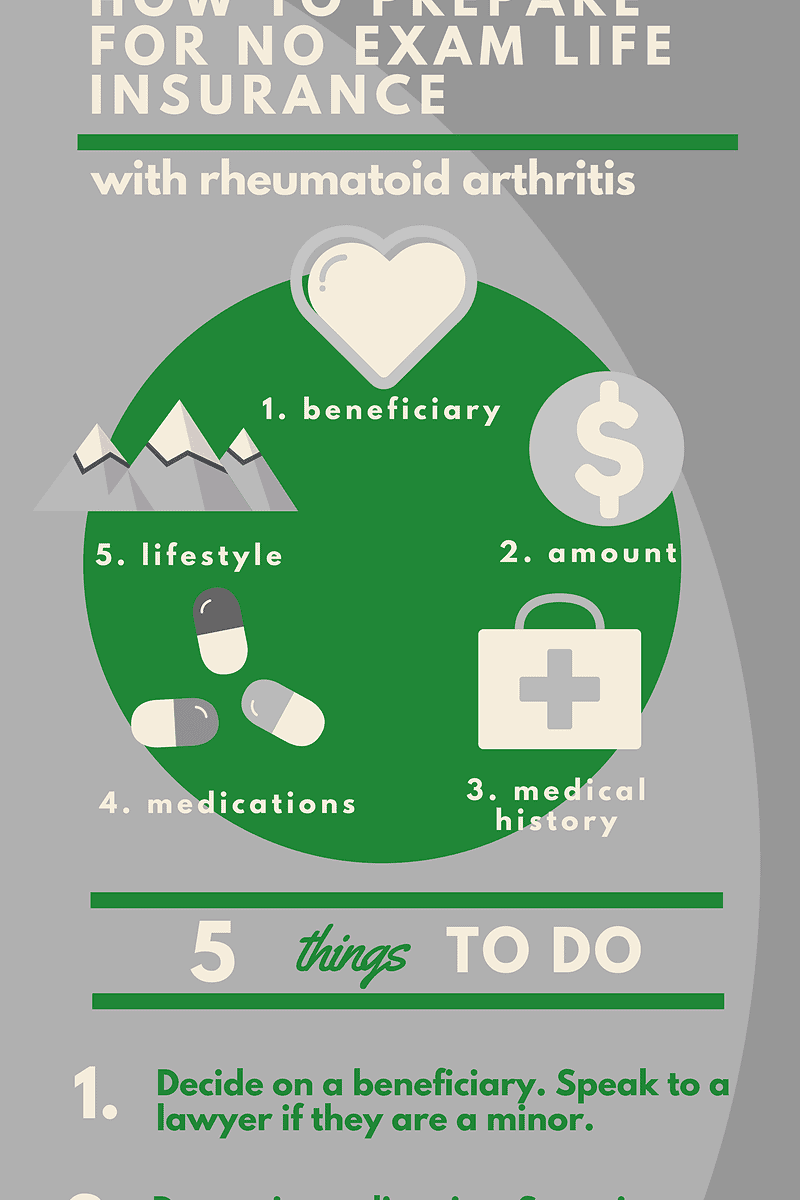

How To Prepare To Purchase A No Exam Policy

If you plan with the following five steps, you’ll be ready to purchase no exam life insurance:

- Decide on a beneficiary – experts will tell you this is the most important decision you will make during your life insurance purchase. Keep in mind:

- Your beneficiary must have an insurable interest, meaning that if you were to pass away, he or she would suffer a financial loss.

- You can have more than one beneficiary. And, you can assign different benefit percentages to them.

- As the policy owner, you can change your beneficiaries.

- An estate planning attorney is an excellent resource if guidance is needed.

- Determine policy size and length – your financial needs and wants need to be assessed before deciding on a policy amount. Important – some life insurance is better than none.

- The default recommendation many life insurance agents recommend is to multiply your annual income by 10 to determine policy size. However, everyone’s situation is unique.

- Your policy length (i.e. 10 – 30 years) should last as long as your financial needs will.

- Assess the following for guidance:

- How much debt do I have?

- How much money do I spend every month?

- What are my longterm financial goals?

- Document medical history – life insurance underwriters, even for no exam, will want to know the overall medical history of you and your close family members. Questions about personal or family history typically include:

- Cancer

- Heart or cardiovascular disease

- Diabetes

- Autoimmune conditions

- Kidney disease

- Sleep apnea

- Stroke

- Liver function

- List all medications – be ready to communicate your prescribed medications. No exam life insurance does have a list of flagged medications. If you are taking any of the following medications, no exam life insurance might not be a good fit. Collaborating with an expert agent will help you find the best policy you qualify for. An independent life insurance agent is not held captive to a particular carrier.

- Abilify

- Aripcept

- Coumadin

- Dexamethasone

- Digoxin

- Enbrel

- Haloperidol

- Humira

- Imuran

- Invirase

- Isosorbide

- Lithium

- Lupron

- Methadone

- Methotrexate

- Nitro/Nitroglycerin

- Prochlorperazine

- Quetiapine

- Rebif

- Remicade

- Risperdal

- Seroquel

- Suboxone

- Tamoxifen

- Warfarin

- Zyprexa

- Record lifestyle activities – no exam underwriters want to know how risky your lifestyle is. They will ask about the following:

- Tobacco use

- Driving record

- History of bankruptcy

- High risk hobbies (i.e. scuba diving, mountain climbing)

- Plans for foreign travel

Although it seems impersonal, your medical history, medications prescribed, and lifestyle activities are all used to assess how much risk you carry. The underwriter gathers up the data and calculates if they are willing to absorb your risk and how much they will charge you.

Here’s a practical take on the process: We like to compare underwriting to a big calculator. The more input (risk) you enter into the no exam calculator, the higher the output (premiums) will be. At some point, if you enter in too much risk, the big no exam calculator will read, “does not compute” and we’ll look at other life insurance options.

Apply For Life Insurance

We specialize in working with clients with rheumatoid arthritis find the highest quality protection at the best prices available. If you have RA and are seeking out life insurance coverage, it’s crucial to collaborate with an agent with a deep understanding of RA. At Rheumatoid Life Insurance, our job is to be your advocate. As an independent life insurance agency, we will cross-reference the top-rated life insurance companies to find the best rate for which you can be approved.

To get started, fill out our Instant Quote form.